India’s economy is growing at a rapid pace, yet insurance penetration remains a persistent challenge. Currently, penetration stands at approximately 4% of GDP, which is significantly lower than the global average of around 7%. While this is often described as a single problem of low awareness, I believe it is actually a collection of many different gaps spread across distinct customer segments. To bridge these gaps, we must stop treating the market as a monolith.

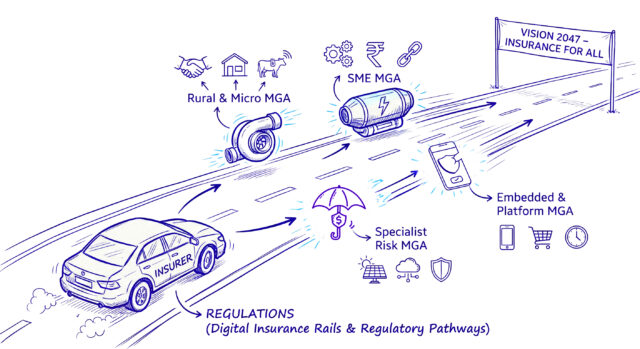

The formal recognition of Managing General Agents (MGAs) under the Sabka Bima Sabki Raksha Bill 2025 is a major step forward. In my view, MGAs should be viewed as the “Innovation Infrastructure” of the market rather than just another distribution layer. They allow for the quick testing of new ideas and data-led products that traditional insurers often find difficult to build within their legacy systems. By allowing MGAs to handle early-stage experimentation, insurers can protect their core business while benefiting from the speed and creativity of focused teams.

To reach the goal of “Insurance for All by 2047,” I believe India needs to develop four specific MGA variants.

1. Rural and Micro MGAs

The main hurdle for rural and micro-customers is the “trust deficit.” These customers often see insurance as a complex product with uncertain benefits. I believe Rural MGAs can solve this by moving beyond simple sales and acting as “community hubs.” Instead of just selling a policy, the MGA should work through local institutions like Microfinance Institutions (MFIs) and self-help groups to manage claims locally.

For example, I think we can move beyond basic livestock insurance toward “Livestock Productivity” models. By using IoT-enabled wearable sensors to monitor cattle’s health, an MGA can trigger a small, preventative payout for medicine if the data shows the animal is falling ill. When a community sees these active, real-time benefits, the trust in insurance increases, making it a visible tool for protecting livelihoods rather than a distant financial contract.

2. SME MGAs

Small and Medium Enterprises (SMEs) are the backbone of our economy, but most are underinsured because standard “package” products do not reflect their actual business risks. I believe the focus for SMEs should shift from basic fire or theft cover toward “Operational Resilience.”

One way to achieve this is through “Pay-as-you-Grow” models. For instance, an MGA could integrate with an SME’s GST or digital payment data to collect tiny premium amounts from every transaction. This ensures that the insurance cost scales naturally with the business’s revenue. Furthermore, I believe we can use supply chain data to offer liquidity protection. If a textile SME’s key supplier is affected by a flood in another state—verified by public weather data—the MGA could trigger an immediate cash flow payout to help them source from elsewhere, keeping the business running without waiting for a physical survey.

3. Specialist Risk MGAs

As India moves toward green energy and a more digital economy, we face new risks that traditional models struggle to address. I believe we need Specialist Risk MGAs that use advanced analytics to provide parametric solutions.

A relevant example for India is “Solar Yield” Insurance. As we scale our solar capacity, plant owners face the risk of low power generation during heavily overcast weeks. A specialist MGA can offer a policy that pays automatically based on satellite data for solar irradiance. Similarly, in the technology sector, a “Digital Trust” MGA could protect SaaS startups. If their cloud infrastructure goes down, the MGA could trigger an automatic payout to the startup clients to compensate for the service interruption. This moves insurance from a reactive claim process to an automatic, data-driven response.

4. Embedded and Platform MGAs

For urban, digitally savvy consumers, the issue is not a lack of awareness but a lack of convenience. In my view, the next evolution for this segment is “Lifecycle-Triggered Protection,” where insurance is woven into the apps people use every day.

We can move beyond simple “sachet” travel insurance by creating products that respond to real-time activity. For example, I believe an “Active Life” MGA could integrate with a user’s wearable health tech. Instead of a fixed premium, the coverage could be tied to physical activity—rewarding a healthy lifestyle with increased critical illness cover. On the other hand, a policy could be designed to “spike” or activate higher accidental cover specifically when a user is detected as traveling at high speed on a highway. This is insurance that follows the risk in real-time, providing protection exactly when and where it is needed most.

From Theory to Action

Recognizing these four variants is only the first step. To unlock their full potential, I believe we need a deeper structural shift in how we approach regulation and shared infrastructure.

Risk-Based Regulatory Pathways

We cannot regulate a rural micro-insurance MGA in the same way we regulate a complex cyber-risk MGA. I suggest that the IRDAI create differentiated regulatory tracks where the level of oversight is matched to the complexity and impact of the product. Lowering the compliance burden for low-ticket, high-impact rural products will allow innovation to flourish where it is needed most.

The “Digital Insurance Rails”

To scale these models, we need a shared digital governance layer—what I call “Digital Insurance Rails.” I propose a system of common APIs and a centralized consent framework that allows MGAs and insurers to exchange data securely and transparently. In the same way that UPI revolutionized payments by providing a common language for banks and fintech, these “rails” would reduce the time it takes to launch a new partnership from months to weeks, allowing the market to react faster to emerging needs.

Outcome-Based Incentives

Finally, I believe we must align business incentives with our national priorities. The government and regulator could offer recognition or “Inclusion Credits” to insurers who provide capacity to MGAs operating in the Rural and SME variants. By rewarding outcomes like “first-time insured users” or “MSME resilience,” we can ensure that innovation is guided by purpose, not just profit.

Conclusion

The path to “Insurance for All by 2047” requires us to match our market structures to the actual needs of our people. I believe that if we embrace these four MGA variants with discipline and clear intent, we can move from “doing more of the same” to building a truly resilient India. By aligning our technology and regulations with the way Indians live and work, we can deliver protection that finally keeps pace with our nation’s growth.

Ultimately, the true measure of our success will not just be a higher penetration percentage or a larger GDP contribution. It will be the number of small business owners who survive a supply chain crisis, the rural families who no longer fear medical debt, and the digital entrepreneurs who can innovate with confidence. If we build these foundations now, we aren’t just selling policies—we are securing the future of a modern India.