Insurance companies are spending more on technology than ever before. Global insurtech investment reached $14.4 billion in 2023, and nearly 78% of insurers are expected to increase their technology investments in 2025. Yet despite this momentum, many insurers continue to struggle with fragmented workflows, disconnected systems, and transformation initiatives that feel painfully slow.

The industry’s biggest challenge today is no longer access to innovation. It is the growing complexity created by buying too many disconnected tools without redesigning the operational foundation beneath them.

Across the global insurance market, technology investments continue to rise aggressively. AI adoption is accelerating, embedded insurance ecosystems are expanding, and insurers are modernizing everything from claims processing to customer engagement. On paper, the industry appears to be moving rapidly toward a more digital future.

But beneath that momentum lies a quieter reality many insurers are beginning to experience firsthand. In fact, 37% of insurers admit to adopting technology without fully understanding its relevance to their business needs, while nearly 60% struggle to move successful pilots into scalable production environments.

The problem is no longer whether technology exists. The problem is whether insurers are implementing technology in a way that genuinely improves operational agility rather than adding another layer of complexity to manage.

For years, modernization efforts across insurance have followed a familiar pattern. A claim inefficiency emerges, and a claim automation tool is introduced. Distribution slows down, and a portal is added. Fraud leakage increases, and AI-based detection tools are deployed. Customer engagement weakens, and another communication platform enters the ecosystem. Individually, these decisions make sense. Collectively, they often create fragmented operating environments stitched together through integrations, workarounds, and manual dependencies.

What started as modernization has, in many organizations, evolved into technology sprawl. Many insurers today are running highly digital customer experiences on top of disconnected internal architectures. The front-end experience may look modern, but underneath, operations remain fragmented across systems, workflows, and teams.

The result is an industry where technology stacks continue to grow, but operational simplicity remains elusive.

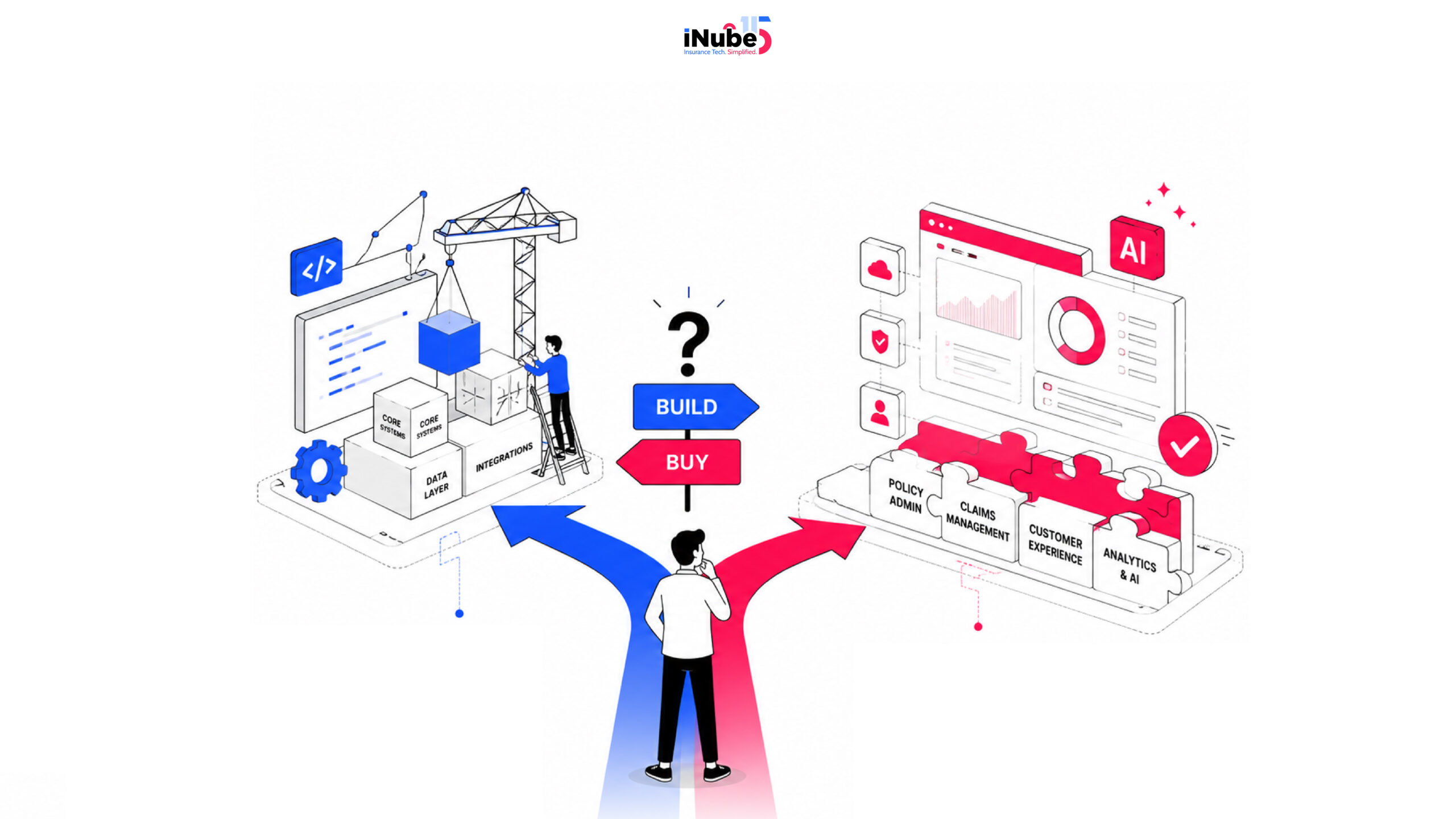

Build vs Buy Is No Longer a Procurement Debate

This is where the Build vs Buy debate becomes far more important than a technology procurement decision. It becomes a question about operational philosophy.

The insurance industry has historically leaned toward building internally in pursuit of customization and control. Nearly 48% of insurers still prefer in-house technology development despite increasing pressure around speed-to-market, integration complexity, and long-term maintenance overheads.

In reality, many internally built systems eventually become operational burdens rather than differentiators. They require continuous maintenance, depend heavily on internal engineering bandwidth, slow down product evolution, and make integrations increasingly difficult over time. What begins as a customization advantage often turns into long-term rigidity.

The larger issue is that insurers are still trying to build capabilities that are no longer true for competitive differentiators. Claims infrastructure is not a differentiator. Policy administration plumbing is not a differentiator. Workflow orchestration alone is not the differentiator.

What increasingly separates market leaders from laggards is the ability to adapt faster, launch products quicker, integrate ecosystems more seamlessly, and create operational responsiveness at scale. Competitive advantage today comes from underwriting intelligence, distribution innovation, customer experience, and organizational agility.

That shift fundamentally changes how insurers should think about technology investments.

The smartest insurers are no longer asking, “What can we build ourselves?” They are asking, “What should we truly own, and what should become part of a flexible operational foundation?”

Technology ROI Depends on Operational Absorption

This is why modular and platform-led approaches are gaining momentum across the industry. Not because buying software is easier, but because operational adaptability has become more valuable than system ownership. Insurers increasingly need technology foundations that can evolve continuously with regulatory changes, new distribution models, embedded ecosystems, AI capabilities, and changing customer expectations.

Technology today is no longer judged only by features. It is judged by how effectively an organization can absorb and operationalize it.

Can teams adopt it effectively?

Can workflows evolve around it?

Can it scale beyond a pilot program?

Can it reduce operational friction instead of introducing additional complexity?

Can it coexist with existing systems without creating integration fatigue?

These are now boardroom questions, not IT questions.

More than 50% of failed insurtech initiatives lacked a clear strategic roadmap at the outset, while 74% of insurers still operate on legacy systems that were never designed to support modern API-driven ecosystems.

The insurance industry has become exceptionally good at experimenting with innovation. Moving innovation from pilot to scalable business value is where many organizations still struggle. AI is perhaps the clearest example of this gap.

Across the market, insurers are rapidly introducing AI into claims processing, fraud detection, underwriting workflows, customer servicing, and operational automation. The pressure to accelerate AI adoption is understandable. AI-driven claims operations are already reducing approval timelines significantly, while fraud detection accuracy has improved by nearly 50% compared to traditional rule-based approaches in some implementations.

The technology itself is advancing rapidly. The challenge is that many insurers are layering AI onto fragmented systems, disconnected data environments, and inconsistent workflows.

AI cannot fix operational fragmentation. It accelerates whatever operational structure already exists. If workflows are disconnected, AI often creates faster disconnection. If data quality is inconsistent, automation amplifies inconsistency. If operational architecture lacks cohesion, technology investments struggle to generate enterprise-wide impact.

The Future Belongs to Connected Insurance Businesses

This is why the next phase of insurance modernization will look very different from the last decade. The winners will not necessarily be the insurers with the largest technology budgets or the highest number of tools deployed across departments. They will be the insurers that reduce operational friction across the value chain.

With nearly 47% of insurance buyers now relying primarily on digital channels, operational adaptability is quickly becoming a business necessity rather than a modernization initiative.

The conversation is gradually shifting away from how much technology an insurer owns toward how connected, adaptable, and scalable the operating model behind that technology truly is.

That distinction matters because insurers today are no longer competing against lack of digitization. They are competing against operational complexity itself.

And in that environment, modernization cannot become the accumulation of disconnected vendor decisions. It must become a deliberate architectural strategy aligned to business outcomes, operational flexibility, and long-term scalability.

The future of insurance will not belong to organizations that simply adopt more technology. It will belong to organizations that create connected businesses around the right technology foundation.

Technology alone will not modernize insurance. Operational clarity will.